Good news for California taxpayers – for taxable years beginning on or after January 1, 2012, California has reinstated the Net Operating Loss (NOL) deduction and the NOL carryover deduction. There is no longer a limitation on the taxpayer’s taxable income for which NOL is available.

Please refer to my previous post on California NOL suspension for the history of this matter, Net Operating Losses – Complexity in California.

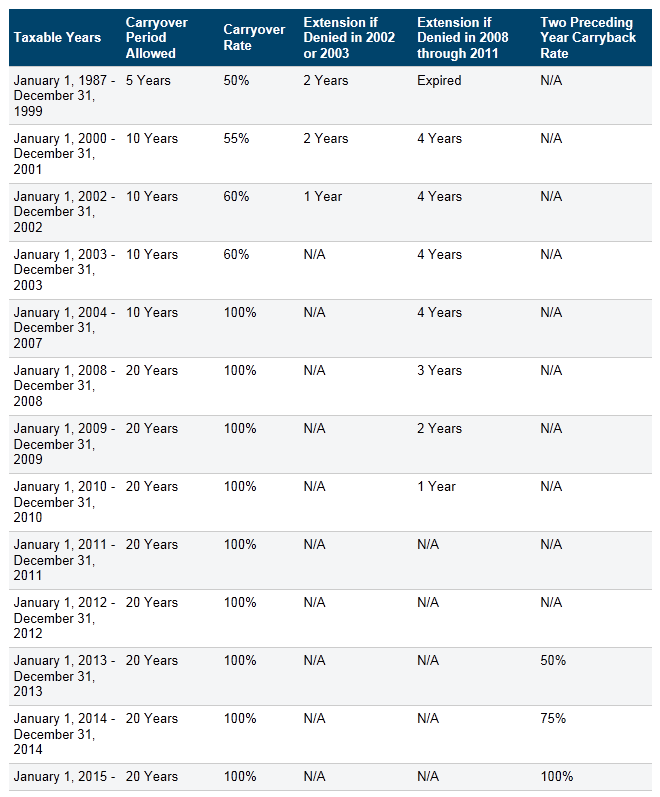

Under the California NOL suspension provisions, the carryover period for each year’s NOL is extended only where an NOL deduction is denied, in whole or in part, because of the application of the suspension provision to that year’s NOL. As the rules on CA NOL keep changing, the table below, provided by the California Franchise Tax Board (FTB) in their article, Clarification of Net Operating Loss Suspended Carryover Period, may become handy when you are determining the rules for any particular year in question:

NOL Limitations

NOL Limitations

For CA NOLs attributable to taxable years beginning after January 1, 2013, a carryback is allowed for the first time and is limited to two years. However, there is additional percentage limitation to the carryback amounts for taxable years 2013 and 2014.

For many taxpayers it is a great relief to be able to finally use their long suspended net operating losses against their income and hopefully retain more cash for their current business operations.