What is Benford’s Law?

Given a large population of numbers, what percentage of the time would you predict each leading digit (1 through 9) would appear first in the list? After thinking through the ways this might be a trick question, most people would still guess that the probability for each would be close…about 11%.

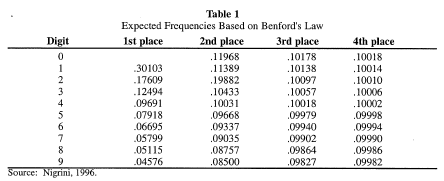

Well…apparently “laws” apply to numbers too! Consider Benford’s Law (also called the “first-digit law”). In the 1930s, Frank Benford, a physicist, noticed that lower digits occurred more frequently than the others because there were more numbers with low first digits in the world. While the probability of occurrence can be expressed by a complicated mathematical logarithm, the essence is that digit one is much farther from digit two than digit eight is from digit nine. Using the mathematical formula, Benford’s Law can be translated for not only first digits, but also for successive digits. Following is Table 1 to illustrate:

Notice the 1st place column. The first digit of one occurs in approximately 30% of the instances; two occurs in approximately 18% of the instances; three in approximately 12%, and so forth. Then notice the 2nd, 3rd and 4th place digits. Amazingly, the successive digits evolve to a more normal probability of about 10% each.

How does Benford’s Law help to detect fraud?

Consider that most people believe in a normal (equal) distribution of first digits. Would knowing Benford’s Law perhaps be useful in discovering fraud? Absolutely! Digital analysis such as this has become a key fraud investigation tool in the recent decade.

Most accounting data can be expected to conform to a Benford distribution. This is true because accounts consist of transactions that result from combining numbers (e.g. invoices result from units multiplied by prices), and large populations (where this analysis is more accurate) can be analyzed.

On the other hand, some populations of accounting-related data do not conform to Benford’s law, such as assigned sequential or other number schemes influenced by human thought. Assigned numbers, for example, should follow a uniform distribution. Also, consider pricing bias for psychological barriers (like $1.99) and ATM withdrawals in pre-assigned amounts. But for naturally occurring number populations, evaluating results in terms of Benford’s Law can be a powerful predictor.

Despite its limitations and the possibility of false positives from using Benford’s Law to analyze accounting data, its usefulness for detecting accounting fraud is supported precisely because naturally occurring numerical data does not conform to conventional thought, which is what fraudsters would use when manipulating numbers to cover up their fraud.